We researched Yield Financial Planning and its competitors, then built the ad scripts, VSL, email sequences, and funnel pages below - yours to use today. Our offer: install and manage it for you on a pay-per-result basis.

Before writing a word, we audited your positioning, competitive landscape, and audience signals. Three findings shaped every deliverable below - and none of it is templated.

Your edge: Founder James McFall is a 2x Top 3 Certified Financial Planner in Australia (2018, 2020) and 2025 Practice Principal of the Year. That thread runs through every piece of content below.

We analysed 5 direct competitors and studied what they're running. The scripts we built position Yield Financial Planning differently.

The #1 thing on their mind before they book: I think I should have an SMSF but I don't know if I actually qualify (balance, complexity, time). Every piece of content below addresses it.

Every piece is finished, written in your voice, and yours to keep regardless of whether we work together. Summary first, then the full text of each piece further down.

Offer: "Is an SMSF Right For You?" Free Strategy Call with Yield Financial Planning

Estimated length: 9-10 minutes

First up, thanks for booking your call. It's a real step, and it tells me you're at least curious whether your super could be working harder than it does right now.

What happens on the call is probably not what you're bracing for. It's a genuine diagnostic, and we mean that literally. One of our SMSF advisors gets on the phone or a video call with you for about half an hour, we go through your balance and your goals, then look at whether property's part of the picture for you. By the end you'll have a straight answer on whether a self-managed fund actually suits your situation, and if it doesn't, we'll say so. We tell people no more often than most advisors would care to admit, because we're fee for service, so we don't earn a cent by talking you into a product that doesn't fit.

You should already have a confirmation with your time and the link to join, so keep an eye out for that. Over the next few days we'll also send you a couple of short emails. They answer the questions that come up on almost every one of these calls, so nothing catches you off guard when you actually speak with the team.

Before then, the most useful thing you can do is sitting right below this video. There are a handful of short clips on the questions nearly everyone asks us, things like what an SMSF really costs all in, or whether your balance is even at the point where it makes sense, or how property inside super actually works. Have a look through the ones that matter to you. That way we're not spending the call covering the basics, and we can put the whole half hour into your situation instead.

Watch a few of those, bring your real numbers, and one of our advisors will take it from there on the call.

When you get on the call there are a few things worth having in front of you, mostly so the first 10 minutes aren't spent digging around for numbers.

The big one is your super. Whatever you've got, including those old industry fund accounts most people have half forgotten about, and your partner's too if you're looking at this as a couple. The easiest thing is to log into the portals beforehand so the team can see the real balances live instead of working off rough guesses.

If you already have an SMSF that an accountant set up for you and you're not sure the strategy's right, dig out the trust deed and the last annual return, and have a rough sense of what's actually invested in there today.

Property works the same way. For anything you own, inside super or out, your advisor will want the rough value, whether there's a loan against it, and what type it is, whether that's residential, commercial, or the premises your own business works from. That matters enormously the moment the conversation turns to moving property into super or buying inside the fund.

And if you run a business or hold a senior professional role, the full financials can stay where they are. They only need to know how it's structured, whether that's a sole trader, a company, or a discretionary trust. Come with those few things and the call can get straight into what the strategy would actually look like for you.

The cost question is the one people are most often uncomfortable getting a straight answer to, so let me put our actual number on the table.

Our SMSF service is an integrated tax and audit service, and the most it'll ever cost you is $2,345 a year. It covers your annual accounting, financial statements, tax return, and the independent audit the ATO requires, all handled in one place. If you'd rather keep your existing accountant in the loop, we'll work alongside them instead. Either way, you'll know the number before you start.

Above that sits the strategic advice, the part that actually decides what your fund holds and how it's structured. That one is separate, it's fee-for-service, agreed up front as a flat fee or a defined scope, and it's never commission, so there's no product kickback hiding in it.

There's also a one-off cost to establish the fund, and that depends on how involved the setup is, particularly if property or borrowing is part of it. We'll quote you the exact figure before you commit to anything, rather than leave you guessing.

Now, set that against an industry fund and the maths gets interesting. At a $1 million balance, an industry fund taking even 0.5% in fees is costing you $5,000 a year, every year, with almost no control over what you're invested in. Push that to $1.5 million and the same fee is $7,500. Once you're above a sensible balance, the SMSF total cost stack often comes in lower than that, and you get full control of what the money's doing.

The team will work the actual maths on your numbers on the call. And if it doesn't stack up for you, they'll tell you, because we only set one up when it genuinely leaves you better off.

Property in super is the conversation that comes up most often, and it deserves a straight answer, because there's genuine upside here and there's also genuine trap territory.

There are 3 kinds of property-in-super that really matter. The one that works best is business real property. That's where you own a commercial premises, your operating company leases it back at market rent, and the rent goes into your retirement fund instead of to a third-party landlord. For trades, clinics, vets, dental, consultancy practices, that's often a great structural move, because the business was going to pay rent anyway, and the related-party rules specifically allow it when the property is genuinely used in the business.

Residential investment property inside super is the next one. It can work, but the rules are tighter. You can't live in it, your family can't rent it, you can't sell your own existing investment property into your SMSF, and the cash flow has to actually stack up inside the fund. We've seen people get talked into this by property spruikers who don't understand the SMSF rules, and that's the trap.

The third is borrowing inside super, the LRBA, or Limited Recourse Borrowing Arrangement. It works for the right asset at the right balance, but the ATO has tightened scrutiny on LRBAs significantly over the last few years, especially on related-party loans and the asset purchase structure, and getting it wrong is expensive.

Yield's edge on property is unusual for a financial planning firm. Our founder holds a Cert IV in Property Services and came through the Property School framework before building Yield, so we advise on the property piece ourselves rather than handing you off to a buyer's agent. Most planners won't touch this work, and most accountants will set the fund up but stop short of telling you whether the property purchase actually makes sense.

Bring your property questions to the call, including the ones other advisors have called too complicated. You'll get a straight read from the advisor you speak with.

Short answer, yes. The longer answer is that expat SMSF work is one of those areas where the structure has to be set up carefully, because the rules around non-resident trustees can catch you out.

There are 2 things the ATO is really looking at. The first is the central management and control test. Broadly, the strategic decisions for the fund need to be made in Australia, or if you're overseas, your absence has to be temporary. The second is the active member test, which looks at where contributions are coming from. If you're working overseas and contributing into the fund from a non-resident position, you can trip this without realising it, and the fund risks losing its complying status, which is an expensive outcome.

We work with expat clients across Singapore, Hong Kong, Britain, America, and Dubai, and the work usually splits into 2 phases. The first is making sure the structure survives your non-residency, which often comes down to how decisions are documented, who's trustee, and the timing of contributions. If you're planning to come back, the second phase is the pre-return CGT and contribution timing work. There are some real wins available in the 12 to 24 months before you re-enter Australian tax residency, and most people miss them because they wait until they're already back.

Time zones we can work around. Bring it up on the call and the team will scope the right approach for your situation.

Fair question, and we won't walk you through a credential wall here. Let me point to the 2 things that genuinely matter for the work we'd do together.

The first is the property-in-super capability. Most financial planners won't advise on direct property inside an SMSF. They'll point you to a buyer's agent or an accountant, and that's the end of the conversation. We do the property work in-house, because our founder holds a Cert IV in Property Services and built the firm around that capability from day one. If property's going to be part of your SMSF strategy, you need an advisor who can actually sit across the structuring, the asset selection, an LRBA where one exists, and how all of that integrates with the rest of your wealth plan. That's rare.

The second is the partnership model. We've been independently owned and fee for service since 2015, so there's no bank behind us and no commission or product quota driving what we recommend. Our NPS sits at 81 plus, which is well above the financial services norm, and it sits there because we're not in the business of one-off advice. We work with clients for the life of their wealth, often into their children's. If you're 50 and looking at the next 30 years of retirement and estate planning, the continuity of who's advising you genuinely matters.

Bring your hardest questions to the call. The team will earn the engagement on the work, not on the pitch.

Subject: Your SMSF call with my team is locked in

Send: Day 1, 5 minutes after booking

Thanks for booking. The calendar invite should already be sitting in your inbox.

If it hasn't landed, have a quick look in your spam, and if it's not there either just reply to this and I'll resend it.

A quick word on what this call actually is, because I'd rather set the expectation now than have you wondering.

It's a diagnostic, not a pitch. My team and I have been doing SMSF strategy work since 2015, and we built the practice so the first call costs you nothing and ties you to nothing. We spend the 30 minutes looking at your numbers, your goals, and whatever structure you've already got, and then I tell you straight whether an SMSF actually makes sense for where you're at.

If it doesn't, you'll hear that from me, and I'll usually point you at the cheaper path that does.

A fair share of the people who book this call walk away with us telling them to stay in their industry fund for now. That's genuinely the right answer for them. Being willing to say so is a big part of why everyone else trusts us with the setup when an SMSF is the right move.

Over the next few days I'll send you a handful of short notes on the things people tend to sit on between booking and the call. What one of these actually costs to run, the balance most people get wrong, how property in super really works, where the accountant stops and the planner starts. Read them or skip them, whatever's useful to you.

Speak soon.

James McFall

Founder & Managing Director, Yield Financial Planning

CFP, Master of Commerce (Financial Planning)

Subject: The real reason people book this call

Send: Day 1, evening (6 hours after E1)

Quick follow-up to the confirmation.

The people who book this particular call tend to look fairly similar. Mid-40s to early 60s, a meaningful super balance built up steadily over the years, often pooled with a partner, a home, sometimes an investment property on top. Most run a business or hold a senior role somewhere. Doctors, executives, IT consultants, lawyers, trades owner-operators.

What's interesting is why they reach out, because it's almost never "I want an SMSF."

It usually sounds more like this. They look at how much super they've got, look at the years left until they stop working, and they don't love how little say they have over any of it. Their industry fund tells them next to nothing about what they're actually invested in. An accountant they've used for a decade has set SMSFs up for other clients but is upfront that they only do the tax return, not the strategy. A bank advisor never really put SMSF on the table, which makes more sense once you realise the bank earns nothing on it.

So they sit there knowing they should probably look into it, and not finding a soul they trust to give them an honest read.

If that's roughly where you are, you're in exactly the right place for this call. We've worked with more than 450 client households sitting in close to that spot, and our Net Promoter Score is north of 81, which is a long way above where financial services usually lands. I mention those numbers not as a brag but as a signal that this is the work we do every single day.

Tomorrow morning I'll send the note on cost, because it's the first thing nearly everyone asks me.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: What an SMSF actually costs to run each year

Send: Day 2, morning

The very first question almost everyone asks me on this call is some version of "aren't SMSFs really expensive to run?"

Honest answer, it depends on the balance. And there's a crossover point where it stops being expensive in any way that matters.

The rough shape is straightforward. Our integrated service, where we handle the tax and audit work alongside the strategy advice, runs to a maximum of $2,345 a year. That's the ceiling, not a starting figure with surprises stacked on top. If you'd rather keep your existing accountant, we work alongside them instead. The setup itself is a one-off, and we quote it on the complexity of your situation rather than slapping a fixed sticker on it, because a clean structure and one with direct property or a borrowing arrangement inside super are genuinely different jobs.

Now hold that next to what you're already paying inside an industry or retail fund.

There the fee is a percentage of your whole balance, and it climbs as the balance climbs. On a $1 million balance at roughly 0.5%, you're around $5,000 a year, with very little control over the mix. Closer to 1% and you're nearer $10,000. Push the balance to $1.5 million and that same 0.5% line is already about $7,500. The percentage keeps marching up with your balance. A largely fixed cost doesn't.

Even so, cost is the wrong lens to judge this on.

People don't move to an SMSF to shave fees, even when that's a happy side effect. They move for control of the strategy, the ability to hold direct property and business real property inside super, and to tie it into the rest of their wealth plan. That's where the real money sits over a 15-year stretch, with compounding doing most of the heavy lifting. Einstein called compounding the eighth wonder of the world for a reason.

Tomorrow I'll go at the balance question directly, because almost everyone gets that number wrong.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: The real SMSF balance threshold (it's lower than you think)

Send: Day 2, evening

Following on from yesterday's note on cost.

You'll still see the old half-a-million rule of thumb floating around plenty of articles, the idea that you need some big round number before an SMSF is worth bothering with. The truth is more nuanced than that, and the figure that actually matters depends on your balance, your member structure, and how complex the strategy needs to be, all read together.

I work from a different number, one tied to where the fee benefits of an SMSF genuinely start to bite.

My own read, and the figure I've written about, is that those benefits become relevant once your balance sits somewhere in the $200,000 to $600,000 range. Below the floor of that, the largely fixed running cost eats too much of your return for the structure to earn its keep. Above it, the maths starts working for you, and it keeps getting better as the balance grows, because the cost stays broadly flat while the balance compounds.

In practice, it tends to play out like this.

I see plenty of people just past $200k who absolutely should have an SMSF and have been sitting on the fence about it for years. I also see a few with much larger balances who honestly shouldn't, usually because their goals are simple enough that a low-fee industry fund beats the SMSF on total return. The balance gets you in the door. Whether you should actually walk through it comes down to strategy.

I'll have a far better read on which side of that line you fall once we go through your specifics on the call. Bring your most recent super statement if you can dig it out, and if you've got a partner who'd also be a fund member, even a rough number for their balance helps.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: How a Melbourne dentist bought his clinic inside super

Send: Day 3, morning

This is the kind of situation we see often enough that it's worth showing you the shape of it before the call.

Take a dentist with a practice in Melbourne's east. Mid-50s, super balance around $850k combined with his wife, who also works in the practice. The business has been paying roughly $96,000 a year in rent to a third-party landlord for the better part of a decade. He's asked his accountant a few times whether he could buy the building inside his SMSF and lease it back to himself, and the answer has always been the same. "In theory, yes, but I don't do that side of it."

When you actually sit down and work the structure, a few things open up.

Business real property is one of the few asset classes where an SMSF can lease the property straight back to a related-party operating company at market rent, as long as the lease is on commercial terms and the paperwork is right. You set up the SMSF, use a limited recourse borrowing arrangement to fund the purchase of a $1.4 million premises, set the lease at independently assessed market rent, and make sure the in-house asset cap and the related-party rules are all satisfied cleanly.

A year on, the practice is still paying its rent. The difference is where that money lands.

It now flows into the couple's own retirement fund instead of a third party's pocket. The building sits in a concessional tax environment too, with capital gains taxed at an effective 10% if it's held more than 12 months, and nothing at all once the fund is in pension phase. On the compliance side, a specialist SMSF accountant co-ordinates with us, so the client is never stuck bridging 2 advisors who don't talk to each other.

None of this is me telling you to go and buy your business premises in super. The point is that the strategy work, plus the borrowing structure and the related-party rules underneath it, are what separate a setup that holds up for the next 20 years from one that lands you in an ATO problem you never saw coming. Get the in-house asset rules wrong, or breach the non-arm's length income rules and cop tax at 45%, and the whole benefit evaporates. Most SMSF setups skip the strategy entirely, which is exactly where that risk lives.

If business real property is something you've turned over in your head, bring it up on the call and we'll run it against your actual numbers.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: Accountant vs financial planner on an SMSF

Send: Day 3, evening

A fair question I get a lot. "My accountant already does my SMSF, so why would I bring a financial planner into it?"

Worth answering plainly.

A good SMSF accountant handles the compliance and admin beautifully. Annual financial statements, member statements, audit coordination, ATO reporting, contribution caps, and the actuarial certificate when there's a pension running. That's their lane, they're essential, and most of our SMSF clients keep their existing accountant precisely because that relationship already works.

What an accountant typically doesn't do, and most of the good ones I deal with will tell you this themselves, is the strategy.

They don't decide what the fund should actually hold, how to think about asset allocation across the SMSF and your personal investments, whether direct property or a borrowing arrangement is right for you, or how the whole thing knits into your tax structuring and your estate plan. That's a different job. It needs an ASIC-licensed financial planner, ideally one who's CFP qualified and SMSF accredited, and ideally one who can hold the property conversation and the tax conversation in the same room.

The way it tends to work in practice is simple enough.

Your accountant keeps doing the compliance and admin, while we take on strategy, investment selection, and the job of tying the whole thing into the rest of your wealth plan, plus the property-in-super work where it applies. We talk to your accountant directly so you're not stuck playing telephone between 2 advisors. Our team carries more than 100 years of combined experience, and we co-ordinate with accountants right across Australia all the time. It's the piece most clients say they wish they'd sorted 5 years earlier.

We can talk through how that split would actually look for your situation on the call.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: The Division 296 change worth understanding before the call

Send: Day 4, morning

Worth flagging one piece of policy before we speak, because it's touching almost every SMSF conversation I'm in at the moment.

The proposed Division 296 tax would add an extra 15% on the earnings attributable to super balances above $3 million, and it's been working its way through parliament. Whether you're near that threshold today or well below it and just watching where you'll be in 15 years, the rule shapes how we think about contribution strategy, what you hold inside the fund, and which assets are better off held outside super altogether.

The reason I raise it now is that I keep meeting people who catch a change like this in passing, panic a bit, and then either over-correct or freeze. Both are expensive.

The right move is calmer than either of those. You model your own trajectory, factor the proposed rules in, and adjust with a clear head. For most people sitting some distance below that threshold, the practical impact over the next 15 years is a good deal smaller than the headlines make it feel, and the SMSF structure itself often gives you more room to respond, not less.

This is the sort of thing we touch on naturally during the call when it's relevant to you. You don't need to read up on it beforehand. I just wanted you to know we'll deal with it directly if your trajectory puts you anywhere near that number.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: A quick note on bank-aligned advice

Send: Day 4, afternoon

One more bit of context before we speak.

A fair few people on this call have already sat down with a bank-aligned advisor at some point, NAB Private, Westpac Private Wealth, Commonwealth, that tier, and they want to know how we're any different. Worth being straight about it.

However nice or knowledgeable your bank advisor is, they're employed to sell bank product. I don't say that as a dig at them as people, it's simply how the institution is built. The product shelf is constrained, the incentives line up with the bank's own funds and lending, and SMSF advice in particular is something most bank advisors won't lead with, because the bank earns nothing on it the way it does on everything else.

Yield was set up in 2015 as the opposite of all that. Independently owned, fee for service from the first day, no commissions, no product to push, no bank parent sitting behind the advice.

We hold the FAAA Professional Practice designation, which is the industry's ethical-practice standard, and we've twice been named Top 3 Certified Financial Planner in Australia, in 2018 and again in 2020. I mention the awards not because they change anything about your situation, but because they mean the work has been independently picked over and held up. Our 450-plus active client households are the more telling signal.

I raise all of this because the SMSF conversation lives or dies on trust. If you can't trust that the advice is genuinely in your interest, the strategy barely matters. We built the practice around exactly that.

See you soon.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: A few practical notes for our call

Send: Day 4, 3 hours before the call

Looking forward to speaking later today.

A few practical notes so we make the 30 minutes count.

Bring your most recent super statement if you can dig it out, plus a rough idea of your partner's balance if they'd also be a fund member. If you've got an accountant who handles tax for your business or your personal returns, it helps to know their name and roughly how that engagement runs. And if there's a specific thing driving the question for you, a property you've thought about buying in super, a business premises lease coming up, an inheritance, a sale event, an expat return, just have it in mind. No documents required. A rough sense of where things sit is plenty.

On the call itself, I or one of my senior team will go through your numbers, your goals, and the structure question, and you'll come away with a clear yes or no on whether an SMSF is the right move for you, plus the next step if it is. If it isn't, you'll know exactly what to do instead.

If something urgent crops up and you need to shift the time, just reply to this and we'll find another slot this week.

Talk shortly.

James McFall

Founder & Managing Director, Yield Financial Planning

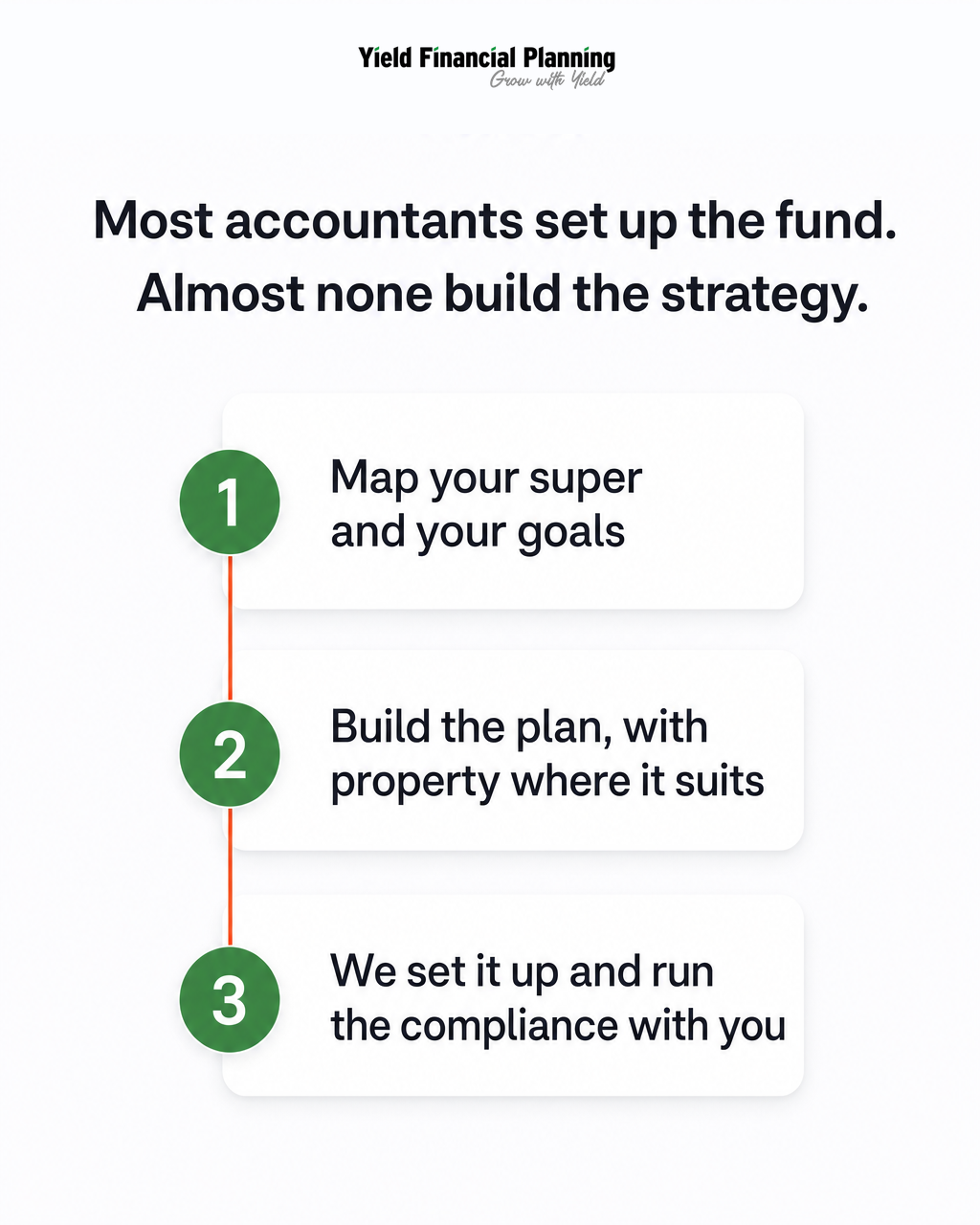

Subject: The SMSF gap your accountant won't fill

Most people assume their SMSF is set up properly because an accountant did it. Fair enough, on paper.

But setting a fund up and running one well are 2 completely different jobs, and most people only ever paid for the first.

Your accountant lodges the deed, sorts the trustee structure, registers it for tax, and files the return every year. They do that part well. Everything that comes after is where the real money in a fund gets won or lost, and it tends to just sit there untouched.

I've run my own SMSF for over a decade and advised on hundreds more, and this is still the thing that catches good people out.

The fund itself is a strategy vehicle. Setting it up is maybe 5% of what it's worth to you. The rest is the part most accountants won't go near, because it was never their job: when to switch on a pension and whose account pays for it, how to hold property without tripping the related-party rules, how it all lines up with your family trust and your business.

I see the same fund walk in over and over. Someone's had it 6 or 7 years, the balance has grown nicely, and the only paper in the file is the annual return and the audit.

No investment strategy worth the name, no contribution plan that maps to what they actually earn, and nothing thought through for the year they turn 65 and everything changes. That last one alone can cost six figures.

None of that's the accountant's fault. They answered the exact question they were asked, and it was a narrow one. Nobody ever told the trustee that someone else was meant to be doing the rest.

So the test is simple. If your fund is worth more today than the day you set it up, and you've never sat down with an advisor to map out the next 10 years of it, your strategy layer is missing.

And it's usually the most expensive thing in the fund.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: Paying rent to a landlord vs paying it to yourself

There's a rule a lot of business owners qualify for and almost none of them ever use. You can hold the building your business trades out of inside your own super.

In plain terms, if you own a trading business, your operating company leases its premises from your SMSF. So your fund owns the building, your business pays market rent into the fund, and that rent is tax deductible to the business on the way out. The income lands in the concessionally-taxed super environment, and the capital growth on the property compounds inside the 15% rate rather than the 30% one your company would otherwise wear.

Now think about what most business owners are already doing. They're paying rent every month, except it goes to a third-party landlord who pockets that rent and keeps the capital growth on top.

Section 71(1) of the SIS Act and the business real property exception are what let that money stay on your family balance sheet instead of walking out the door for good. I've watched owners do this for 15 years and end up owning their premises outright inside super, and I've watched plenty more pay a landlord for the same 15 years and own nothing.

There are a few conditions worth knowing before you get too excited, and I'd rather you heard them from me than found out on audit.

The property has to be used wholly and exclusively in one or more businesses. Mixed-use gets messy fast, and residential dressed up as commercial tends to get knocked back when the auditor looks closely.

The lease has to be at arm's length too. That means genuine market rent, market conditions, paid on time, with a real lease document sitting behind it. Underpay it to help cash flow and you've got a problem, overpay it to tip money in and you've got a different one.

And if the SMSF borrows to buy the property, that borrowing has to sit inside a Limited Recourse Borrowing Arrangement. It's technical, the lenders are fussy, and the rules tightened again in 2024.

So why is something this good still rare. It needs 3 professions actually pulling in the same direction, with your accountant on the entity side, a planner like me on the SMSF and contribution side, and a property lawyer on the lease and the LRBA paperwork. Most owners can't find all 3 talking to each other, so the conversation never even starts.

If you own your business and you're writing a rent cheque to someone else every month, that's the cheapest hour of advice you'll buy all year.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: A $180,000 SMSF mistake I've watched happen in slow motion

This is the kind of thing that lands on my desk for a second opinion most years, and the pattern barely changes.

Picture a business owner in his late 50s with a super balance just over $1.4 million. He's had the SMSF for 9 years, set up by an accountant he likes and trusts. The fund holds cash, some Australian shares, and a residential investment property he bought 5 years ago with an LRBA.

Then he gets offered a price on the property well above what's left on the loan, and he decides to sell.

The accountant's advice sounds sensible - sell, pay out the loan, bring the cash back inside super.

This is where it gets expensive. Before he signs a thing, there are really only 3 questions that matter. Has he actually checked his concessional contribution position over the last 5 years, including any carry-forward cap he never used. Is his wife a member of the fund yet. And has he switched on a pension phase account for any of it.

In a case like this, 9 times out of 10, the answers are no, no, and no.

Run the accountant's version and he realises a six-figure capital gain sitting in the fund's accumulation phase, taxed at 10% after the discount, with nothing to offset it. That's real money gone, on a decision that looked completely obvious at the time.

Now look at what you'd do with the same fund over a fortnight. First his wife comes in as a second member. Then you redirect his unused carry-forward concessional contributions so you're using both their caps, not just his. And you time the sale so part of the gain lands in pension phase for him and part in accumulation for her. On numbers like these, the CGT outcome can swing by roughly $180,000 in his favour across the eventual draw-down.

The accountant wasn't wrong, and I want to be fair to him. He answered the question he was asked, which was how to sell the property. Nobody ever sat him down and asked the real question, which is how to fund the next 25 years of this bloke's retirement out of that one asset.

I see versions of this every single year. The fund almost never goes wrong at setup. It goes wrong on the one or 2 big moves it makes across its whole life, the property sale, the contribution call around 65, the day someone flicks on pension phase. Those moves get made on autopilot, and the autopilot tends to cost six figures.

So if you've got a property in your SMSF and you're inside 5 years of selling or retiring, this is the conversation to have now, well before there's a contract on the table. Reply and I'll take a look at where your fund actually sits.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: What the ATO is looking at in your SMSF this year

The ATO has gone fairly public lately about where it's pointing its SMSF compliance attention. None of it's new law. What's changed is the appetite to enforce it, and a few areas are now worth a proper look from any trustee carrying a decent balance.

Start with non-arm's length income. If your fund earns income from a related party on terms that are sweeter than market, the ATO can tax that income at 45% instead of 15. Read that again, because the gap is brutal. The classic trap is a cheap lease rate on business real property, or a loan from a director into the fund priced too low to be real. Since 2021 they've stretched how they read NALI to catch expense shortfalls too, not just inflated income, and that interpretation has been grinding through the system ever since.

Then there's the LRBA paperwork. Funds that borrowed before 2018 under the old safe-harbour rules have been told to drag their documentation up to current standard. Anyone who borrowed since 2024 is dealing with tighter lender requirements on top, and auditors are flagging far more of these at the annual SMSF audit than they used to.

The third one is in-house assets, where most trustees know there's a 5% cap but miss the drift over it through capital growth. A related-party investment creeps past the threshold on nothing more than capital growth, and now they're in breach without having done a single thing wrong. The penalty is forced disposal inside the next financial year, which is a horrible position to sell from.

None of this is dangerous if you've kept your fund clean. I'm writing about it because the trustees most likely to get caught are the ones who set the SMSF up 6 or 8 years ago, haven't had a strategy review since, and just assume the annual audit will tap them on the shoulder if anything's off.

It won't. The audit checks that you've complied with the rules. It says nothing about whether your structure is still the right one under the law as it stands today.

So if your SMSF holds property, has borrowed at any point, or has related-party exposure of any flavour, this is a good year to put fresh eyes across the documentation before the ATO does it for you.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: 10 years inside my own SMSF, what actually mattered

I've run my own SMSF for more than a decade now, and Yield has advised on hundreds more over the same stretch. The honest part is that the lessons which actually mattered weren't the ones I went in expecting to learn.

What surprised me most was how little investment performance moved the needle. Markets did what markets always do, compounding ground away in the background, and an asset mix I argued about for weeks in year 2 made almost no difference by year 9. What drove the balance was something far more boring. It was how much I put in, and when. Investment selection rounded the edges, and contribution discipline did the heavy lifting, and I wish someone had hammered that into me at the start.

The second lesson took me longer to admit. An SMSF only earns its keep when you use it for things an industry fund flat out can't do. For me that meant direct property, and the control to time a sale for the tax outcome I actually wanted. If your fund is just holding a handful of large-cap shares and an ETF, you're paying SMSF money for industry-fund returns. Nothing wrong with that mix. It simply doesn't justify the trouble of the structure, and I'd say that to your face on a first call.

My third lesson crept up on me over the decade. The rules keep changing, and almost no trustee notices when they do. We got the transfer balance cap in 2017, then the non-arm's length income expansion in 2021, then LRBA borrowing tightened again in 2024. None of those made the news a trustee would ever read, yet every one of them shifted the right answer for people who already had the structure in place. A fund set up perfectly in 2016 wasn't necessarily set up correctly for 2026.

And the one I really didn't see coming is that an SMSF turns out to be the most useful estate-planning vehicle most families will ever hold, and hardly anyone treats it that way. Reversionary pensions, binding death benefit nominations, how it all knits in with the family trust, the tidy-up that has to happen before the second member dies. The decisions you make in year 9 of a fund end up mattering far more than anything you decided in year one.

After all these years, if I were starting over tomorrow, I'd spend 80% of my thinking on contribution strategy and structural reviews, and 20% on picking investments. Most trustees run that split exactly backwards, and it costs them.

James McFall

Founder & Managing Director, Yield Financial Planning

Subject: The balance where SMSF fees cross over industry super

A quick one, from running the numbers on hundreds of funds over the years.

The point where an SMSF actually gets cheaper than an industry fund is almost never where people imagine it is. Take a balance of around $1 million. At industry fund rates, call it somewhere between 0.5% and 1% all-in, you're handing over roughly $5,000 to $10,000 a year just in fees. A well-run SMSF, with the accounting and audit and advice and platform costs all in, frequently comes in well under that on the same balance.

And the gap only gets wider as the balance grows, because SMSF costs sit pretty flat while a percentage fee keeps climbing right alongside your money. Push the balance to one and a half million and that same 0.5% is already about $7,500 a year, whether the fund earned its keep that year or not.

But that's the easy half of the maths, and honestly it's also the worst reason to run an SMSF. Nobody should take on trustee duty for a fractional saving on fees.

You take it on because you want to do something an industry fund simply can't let you do, like holding direct property, or the building your own business trades from, or timing your own capital gains around when it suits you, or running pension and accumulation phase across 2 members with real precision.

If none of that applies to you, the industry fund is the right answer no matter how big the balance gets, and I'll tell you so. If even one of them does, the fee saving becomes a rounding error next to what the structure lets you build. You'll still hear the old half-a-million rule of thumb thrown around, but in practice the fee benefits start showing up somewhere in the $200,000 to $600,000 range, a fair way below where most people assume.

So the question to put to your advisor isn't "are we saving on fees." It's "what does this structure let us do that the old one couldn't." If the honest answer is nothing, the structure isn't earning its place. If you want me to look at whether yours is, book a quick call.

James McFall

Founder & Managing Director, Yield Financial Planning

Every asset above plugs into one place in this flow. Once it's running, the only thing you see is qualified bookings on your calendar.

We handle every piece of the build, deployment, and the first 30 days of campaign management. You film, we run.

If yours isn't here, it's the first thing we'll cover on the call.